How to actually budget with an offset account (without opening more accounts)

Your offset account is already saving you money on interest. But there's one problem most people never solve: you have no idea what you can actually spend.

The offset account trap nobody talks about

You set up your offset account. You moved your savings across. Your interest repayments dropped. Great.

But now you open your banking app and see $18,400 sitting there. And you have absolutely no idea how much of that is yours to spend.

Is the $1,200 rego coming out next month already accounted for? What about the holiday you're planning? The emergency fund you keep meaning to build?

Most Australians in this situation do one of two things: they open extra savings accounts to separate their goals (and lose the offset benefit), or they just guess — and sometimes get it badly wrong.

Your bank balance is showing you one number. But it's not telling you how much of that is already spoken for. That gap is where financial stress lives.

Why multiple accounts isn't the answer

The classic approach is to split your money: a "bills" account, a "holiday" account, an "emergency fund" account. Each goal gets its own bucket.

The problem? Every dollar sitting outside your offset account is costing you interest. If you have a $500,000 mortgage at 6.2%, every $10,000 you move out of your offset costs you roughly $620 a year in extra interest. Spread $30,000 across three separate accounts and you're potentially giving up close to $2,000 a year.

The whole point of an offset is to pool your money. Splitting it defeats the purpose.

The better approach: one account, full picture

The solution isn't to separate your money. It's to track what it's earmarked for — while keeping everything in one place earning maximum interest.

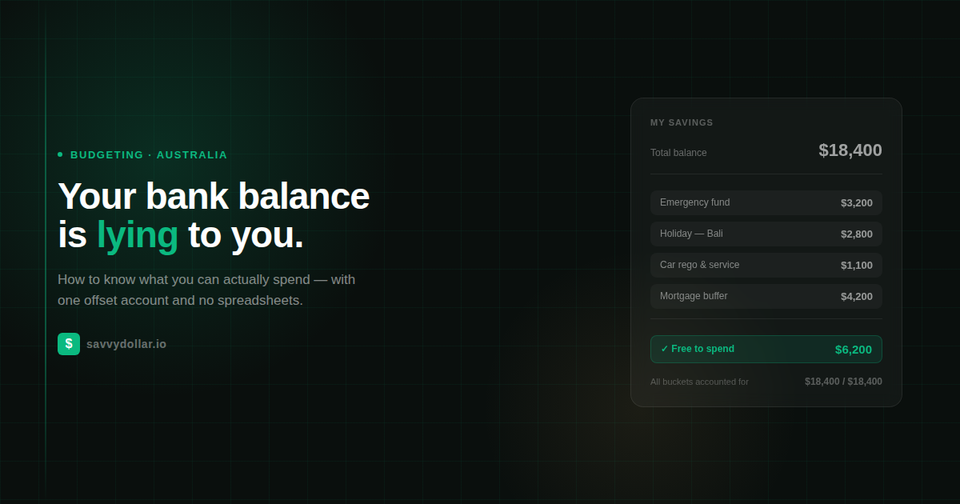

Think of it this way. Your offset account might show $18,400. But here's what that balance actually represents:

Total balance: $18,400 — but only $6,200 is genuinely available.

Now instead of guessing, you know. Every dollar has a job. And your entire $18,400 is still sitting in your offset, working hard on your mortgage.

How to set this up

Step 1: List every financial goal you have right now

This includes irregular bills (rego, insurance, rates), savings goals (holiday, emergency fund, new car), and any buffer you want for the unexpected. Don't overthink it — start with whatever feels most urgent.

Step 2: Work out how much each goal needs

For irregular bills, divide the annual amount by 12 to get a monthly allocation. For savings goals, set a target date and work backwards. For a buffer, a common rule of thumb is 3 months of essential expenses.

Example: Car costs $1,200/year in rego and $800/year in servicing = $167/month to set aside. You don't open a new account for this — you just earmark $167 from your paycheck to your "car" allocation every month.

Step 3: Track the breakdown somewhere

A spreadsheet works fine if you stay on top of it. The main thing is that every time money comes in or goes out, you update which allocation it belongs to. Over time you always know your real spendable balance — not just your total.

If you want this to happen automatically, that's exactly what Savvy Dollar is built for. You connect your accounts, set up your allocations (we call them Buckets), and it maintains the breakdown in real time — so your true spendable balance is always one glance away.

Common questions

What if I don't have enough to cover all my allocations?

That's actually useful information. If you try to set up your allocations and the numbers don't work, it means your income and expenses aren't currently in balance — and it's better to know that now than to find out when rego is due. Start with your most important goals and build from there.

Does this work with a redraw facility instead of an offset?

The same principle applies, but be careful: funds in a redraw facility are technically part of your loan, and some lenders restrict access or charge fees for redraw. An offset account gives you full liquidity, which makes this approach cleaner. If you're on a redraw-only product, this strategy still helps you track what's available — just be aware of the access differences.

How often should I update my allocations?

At minimum, when you get paid. Ideally whenever a significant transaction happens. The more current your breakdown, the more useful your real spendable balance becomes.

The mindset shift that makes it click

Most budgeting advice focuses on restricting what you spend. This approach is different — it's about knowing what you have.

When every dollar is earmarked, you stop second-guessing your spending decisions. You either have the money allocated for something, or you don't. No guilt, no guessing, no nasty surprises.

Your offset account is already doing the hard work of maximising your interest savings. This system gives you the clarity to actually use it with confidence.

See your real spendable balance

Savvy Dollar connects to your accounts and tracks your Buckets automatically — so you always know what's genuinely free to spend.

Start for free — no credit card required →

Comments ()