How to Pay Off Your Home in Half the Time With an Offset Account

If you are a homeowner with a mortgage or are looking at buying a new home, and living in Australia or the United Kingdom, there is a good chance you have heard of an offset account. An offset account is a linked deposit account offered by the financial institution with every dollar saved within that account earning interest at the prevailing rate of your home loan, thus reducing the interest accrued to your home loan at the end of the month. Your balance due on your home loan is therefore offset against the credit balance in your offset account.

Your offset balance remains a liquid asset, meaning the funds won't be capitalised against your loan account and you can access these at any time should you have the need.

The Power of an Offset

An offset account is an amazing tool to reduce interest and the overall cost of home ownership. When used appropriately, it can cut your cost of finance and loan term significantly. At worst you'll take a significant chunk off your overall repayment term and total repayments.

An offset account may not provide you with the highest returns than other investment types can over the long term. There are certainly other investment opportunities with higher risk profiles which are better suited to a long term investment approach.

An offset account will however, provide you with guaranteed returns, immediate access to your cash and an opportunity to increase your equity and reduce your home loan costs and repayment term far quicker than your contractual repayment schedule.

Tax Efficiency

The tax savings on an offset account is one of the key advantages it has compared to other savings and investment types. With an offset account, the interest you save by reducing your home loan balance is not considered income, so you don't pay tax on it.

Therefore, where your marginal tax rate is 35%, to get the same after-tax benefit as a 5% tax-free return from your offset, your taxable investment would need to provide a an interest rate of approximately 7.69%.

Using an Offset

The 3 best ways to use an offset account are:

- Your main income account, i.e., where you receive your salary, rent income and additional income, such as side hustle earnings.

- Your savings account, where you save for the short to medium term and want to eliminate any risk to loss of capital

- Your emergency fund. It's generally recommended that you should have enough money in your emergency fund to cover at least 3 to 6 months worth of living expenses, and this money should be freely accessible in the time of urgent need.

An offset account represents the ideal savings vehicle, providing you with an interest rate equal to your home loan, without locking you in with volatile market pricing or early termination fees.

Running the Numbers

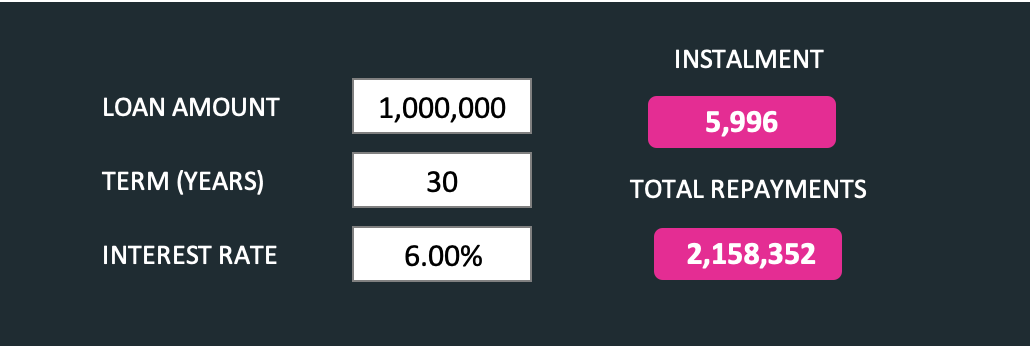

Let's run the numbers, using what some might consider a typical home loan in this current day and age. A $1 million loan with a repayment term of 30 years with a 6% annual interest rate.

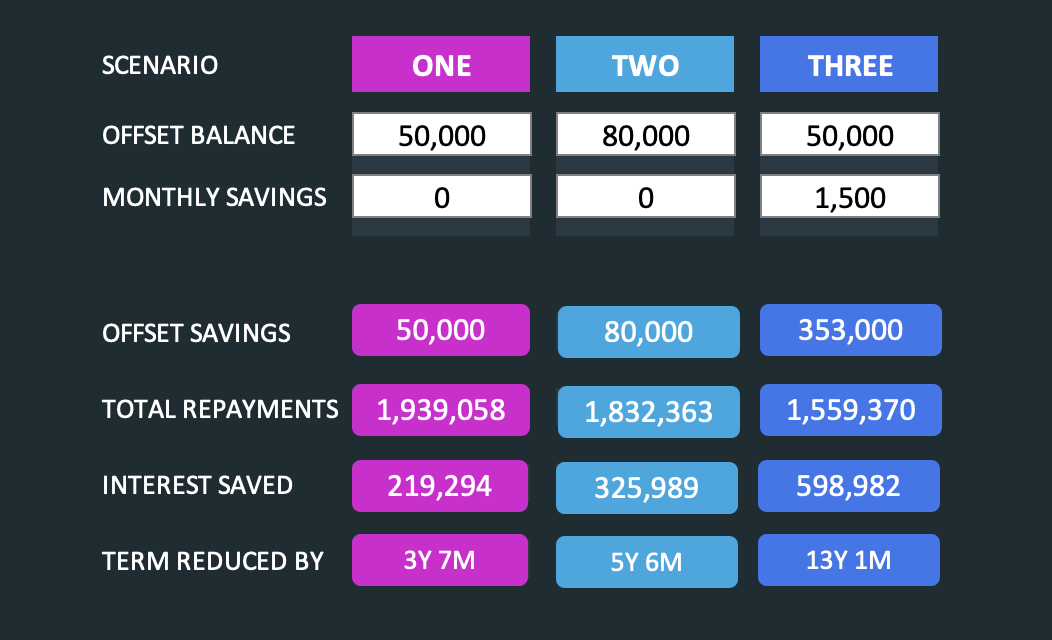

Assuming we have $50K in our emergency fund, or a combination of emergency savings along with our monthly earnings. Over the lifetime of the loan we would save ~$220K in interest and repay the loan earlier by 3 years and 7 months.

If we had $80K, we would save $325K in interest and reduce the loan term by 5 years and 6 months.

If we again had $50K, per the original example, but opted to save $1,500 per month. We would save almost $600K in interest and reduce the term by 13 years and 1 month.

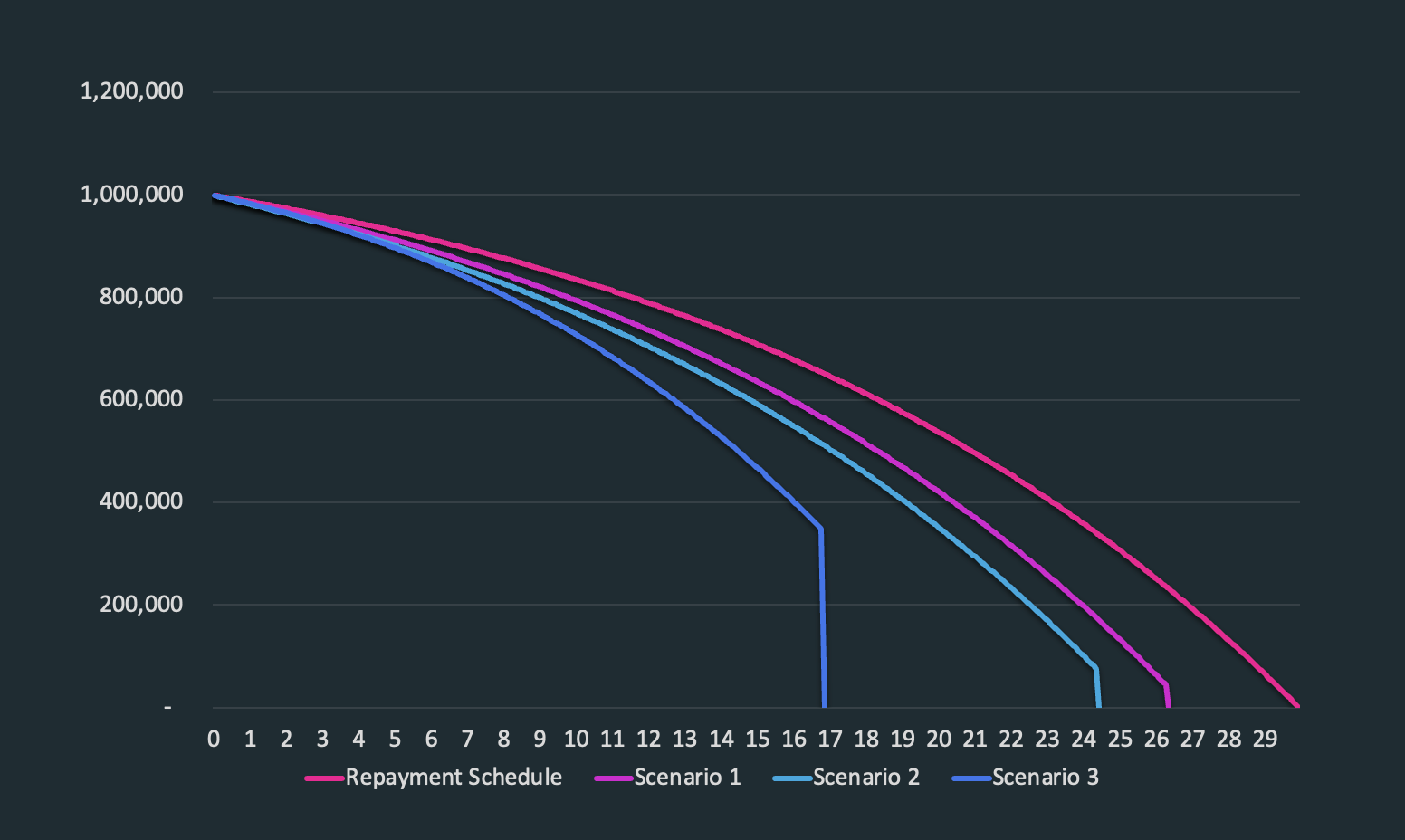

By plotting the outstanding balance of the original loan schedule over time, along with the 3 offset savings scenarios, we can see how significant the reduction in loan term can be and what a powerful opportunity an offset account represents.

Offset vs Savings Account

When comparing an offset to a savings account, in almost all cases the offset is much more beneficial. There is one factor in which you may still prefer to use a savings account, and that is in the case of cash flow. The offset account does not actually reduce your monthly payment on your mortgage, only the interest accrued. The financial benefit is only realised once your loan is settled, either through early payoff or when you sell your property.

For your savings account, every month you will receive the interest earned back into your account, forming part of your total income. This is advantageous particular if that additional income is required to balance your budget.

| Category | Offset | Savings |

|---|---|---|

| Interest Rate | ✅ Linked to higher mortage lending rate | ❌ Always lower than the prevailing lending Rate |

| Tax | ✅ Tax-free | ❌ Interest earned taxed per your marginal tax rate |

| Liquidity | ✅ Savings immediately available | ✅ Savings immediately available |

| Cash Flow | ❌ Earned interest is used to offset mortgage interest | ✅ Earned interest is freely available |

The Bottom Line

In summary, used well, an offset account is a risk-free option to building additional equity in your home, by reducing your interest and paying down your debt much faster. Using it to build up your emergency fund is the first step. Thereafter, continue to make recurring savings deposits to make meaningful reductions in your loan term and total repayments

If you have access to an offset account and not yet using it, start immediately. If you're about to purchase a property and are looking at mortgage options, ensure that an offset account is one of the features that your mortgage lender offers. It will make a significant difference in the long-term.

Comments ()