New Tax Rules Just Tipped the Scales Toward Your Offset Account (2026)

The 2026 Federal Budget just changed the investing calculus for a lot of Australians. If you've been quietly building a share portfolio or stacking ETFs with the assumption that the tax system would reward your patience — you need to reconsider the numbers.

Because right now, your mortgage offset account might be quietly one of the best moves you can make.

Let's break it down.

What just changed with capital gains tax

Australia's 50% CGT discount has been a cornerstone of the investment playbook since 1999. Hold an asset for more than 12 months and only half your gain gets taxed. For someone on a 37% marginal rate, that meant an effective CGT rate of just 18.5%.

That era is ending.

From 1 July 2027, the government is replacing the 50% discount with cost base indexation — adjusting your purchase price for inflation when calculating a gain — and introducing a 30% minimum tax rate on capital gains, regardless of your marginal tax rate.

In plain terms: the tax advantage of investing in shares and ETFs through your personal name just got meaningfully smaller. If your marginal rate is already above 30%, you'll now pay a top-up tax to hit that floor. If you were counting on timing a sale in a low-income year to pay minimal CGT, that strategy no longer works.

Worth noting: these changes apply to gains accruing after 1 July 2027. Assets you already hold retain the 50% discount on gains accumulated up to that date. But for new money you're deploying from here? The game has changed.

The alternative: your offset account

If you have a home loan with an offset account, you're sitting on an investment that the CGT changes can't touch — because it's not a capital gain at all.

Every dollar sitting in your offset account reduces the principal your bank charges interest on. If you have a $600,000 loan at 6.2% and $50,000 in your offset, you only pay interest on $550,000. That's roughly $3,100 a year in interest you never pay — equivalent to a guaranteed 6.2% return.

And here's the part people often miss: that return is tax-free. You're not earning interest income, you're avoiding an expense. The ATO doesn't tax money you don't pay out. No income tax. No CGT. Nothing.

Compare that to the post-2027 world where a share portfolio earning 6.2% annually gets eroded by a minimum 30% CGT hit on your real gains when you eventually sell. The offset's guaranteed, tax-free return becomes increasingly hard to argue against.

Running the numbers: a simple comparison

Let's say you have $50,000 to deploy over the next few years, and a home loan at 6.2%.

Option A — Offset account

- Interest saved per year: ~$3,100

- Tax payable: $0

- After-tax return: $3,100 (6.2% guaranteed)

- Risk: none

Option B — Broad market ETF (historical ~9% average return)

- Gross annual gain: ~$4,500

- CGT on realisation (post-2027, minimum 30%): you pay tax on your real gain above inflation

- After-tax return: varies significantly by holding period and inflation rate, but meaningfully lower than the headline return

- Risk: market-dependent

For the ETF to beat the offset after tax in a post-2027 environment, it needs to consistently outperform the offset return and overcome the CGT drag on realisation. Historically that's been achievable over long timeframes — but the margin has narrowed, especially for investors with higher marginal tax rates.

Short-to-medium term? The offset is increasingly compelling.

So should you ditch investing altogether?

No. This isn't about abandoning investing — it's about being honest about the maths.

Long-term investors, especially those putting money into super (where the CGT environment is very different), still have a strong case. ETFs held for decades with compound growth still build real wealth. And investing through super remains one of the most CGT-efficient vehicles available — a 15% tax rate on earnings, 10% on long-term gains.

But for money outside super, held in your personal name, with a home loan sitting next to it? Your offset account deserves a proper seat at the table.

The old mental model was: offset is boring, investing is where the real returns are. The new CGT environment challenges that assumption directly.

The problem most people have with their offset

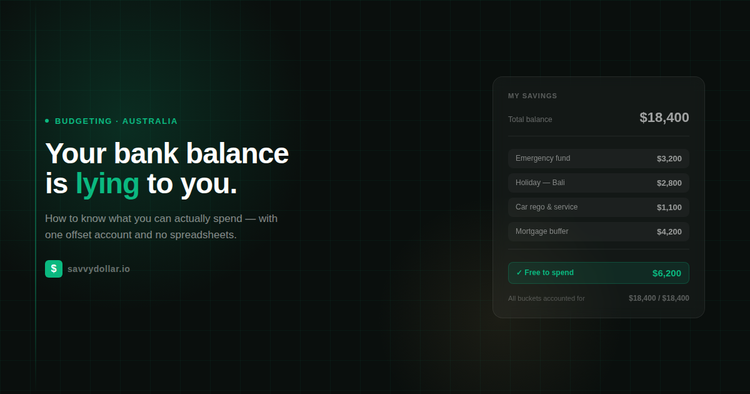

Here's the frustrating part: most people don't use their offset anywhere near its potential.

The offset account earns its keep based on how much money sits in it — and when. But for most people, money flows in on payday and trickles out over the month across rent, groceries, dining, subscriptions, and a hundred other things. The average balance ends up far lower than it could be.

And there's a second problem: people have no idea how much of that balance is truly "free." Is the $22,000 in your offset your emergency fund? Your holiday savings? Next quarter's tax bill? Your renovation deposit? Without clarity, spending feels risky — so people move money out, into separate accounts, and in doing so, give up the very interest savings they were after.

This is exactly what Savvy Dollar is built for

Savvy Dollar's Buckets system was designed to solve this problem precisely.

Instead of fragmenting your savings across five different accounts — each earning worse interest than your offset — Savvy Dollar lets you keep everything in one account (your offset, or any high-yield account) while maintaining complete clarity on what every dollar is earmarked for.

Your emergency fund, holiday savings, tax reserve, and car maintenance fund can all sit in your offset simultaneously — each tracked as its own Bucket inside Savvy Dollar — while the full balance works hard against your mortgage interest every single day.

The result: your offset balance stays higher, for longer, and you know exactly what's genuinely free to spend. No guessing. No shuffling money between accounts. No leaving interest on the table.

If you're reconsidering where your money is best placed in a post-CGT-discount world, the offset is worth a serious look — and Savvy Dollar makes sure you actually capture every dollar of that advantage.

The takeaway

The 2026 Budget changes don't make investing irrelevant. But they do change the comparison.

A guaranteed, tax-free return from your offset is now competing more seriously with the after-tax returns from shares and ETFs held in your personal name. For some people — particularly those with meaningful mortgages, higher marginal rates, or shorter investment horizons — the offset may come out ahead.

The smartest move? Don't treat it as either/or. Build a strategy where your offset is working as hard as possible, your super is investing efficiently in the background, and any investing you do outside those two is done with clear eyes on the new CGT rules.

Get started today!

Ensure your offset is actually earning everything it can That's what Savvy Dollar does best.

Start for free — Savvy Dollar →This article is general information only and does not constitute financial or tax advice. The CGT changes described are proposed legislation announced in the 2026 Federal Budget and have not yet passed Parliament. Speak to a qualified financial adviser or accountant about your specific circumstances before making investment decisions.

Comments ()