Are Early Payment Discounts Worth It?

Earlier this year, I received a Tuition Fee Schedule for my 2 children. I'm blessed with a boy of 11 years and a girl of 6. This schedule contained a breakdown of the total costs for the year, along with the payment due dates for each of their 4 school terms.

Early Payment Discount

In it, there is also a small paragraph stating that should I pay the full-year account before the start of the school year; I would be entitled to a 5% Early Payment Discount.

Now I never really gave this offer much consideration. I had the funds available but also, I had a new and sizeable home loan with a linked offset savings account, providing some interest respite at a rate of 6.39%. I assumed that given the Time Value of Money principle and the higher rate, I was better off holding onto my cash and paying monthly.

In analysing this decision for what was meant to be the original intent of this article, by how much I had benefited from this decision, I realised that I was WRONG! 😮

Calculating the Returns for Each Option

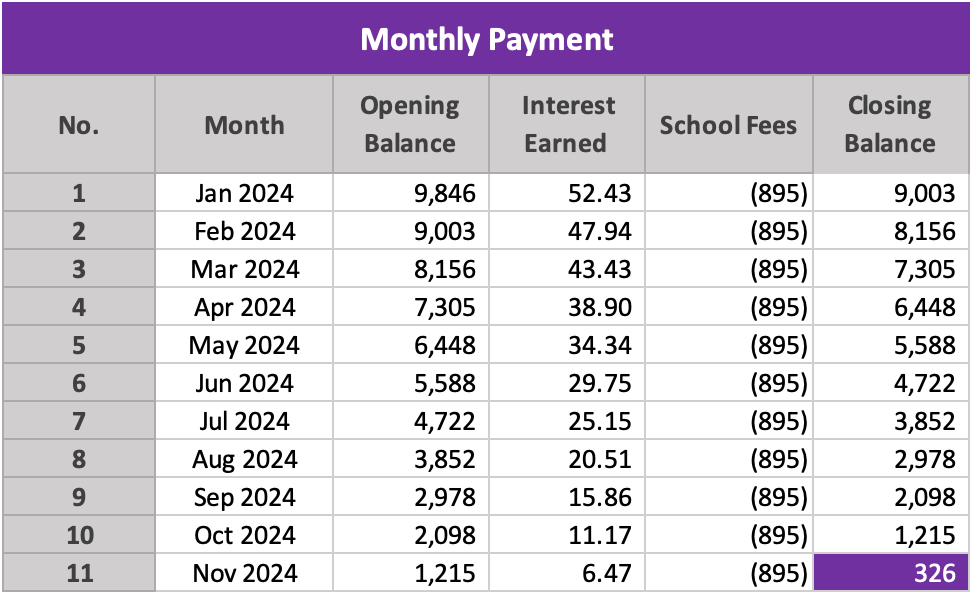

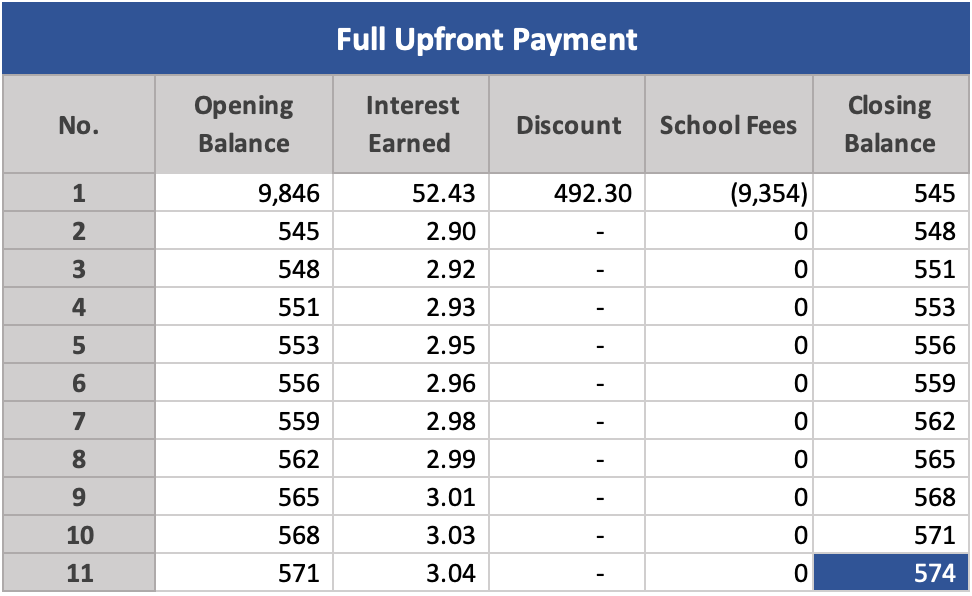

The table below represents my particular scenario. The choice of paying the annual school fees upfront or in 11 equal monthly instalments (Jan - Nov).

I had the funds in hand, sitting in a savings account earning 6.39% interest. This seems like a generous interest rate for a basic savings facility, which it is, however it is only because it's linked to my home loan as an offset account.

| Period | January - November (11 Months) |

|---|---|

| Annual School Fees | $ 9,846 |

| Monthly Repayment | $ 895 (annual fees / months) |

| Early Discount | $ 492 (5%) |

| Savings Interest % | 6.39% |

With both scenarios, the assumption was that these funds are kept in the savings account earning 6.39% interest, calculated daily and compounded monthly,

By modelling out the 2 scenarios (monthly/upfront) on a month-on-month basis; current balance, interest earned, and school fees payable, we can start to understand the interest earning potential of each option.

With both scenarios, the available funds are kept in the savings account earning 6.39% interest, calculated daily and compounded monthly,

It quickly became apparent that for the monthly repayment option, the funds on hand quickly diminished, and with that, the interest-earning potential, as 1/11th of the total amount was reduced each month with each instalment.

For the upfront payment, there was very little interest earned, apart from the first month where the payment was due by at month-end. The value of this option is in the discount received, which continues to be saved and earns approximately $3 per month for the remainder of the term.

Early Discount is the Winner! 🏆

At the end of the 11 months, the Monthly option returns $326 but the Upfront option, providing the early discount, surprisingly betters that by $248, returning $574 in discount and interest.

Comments ()